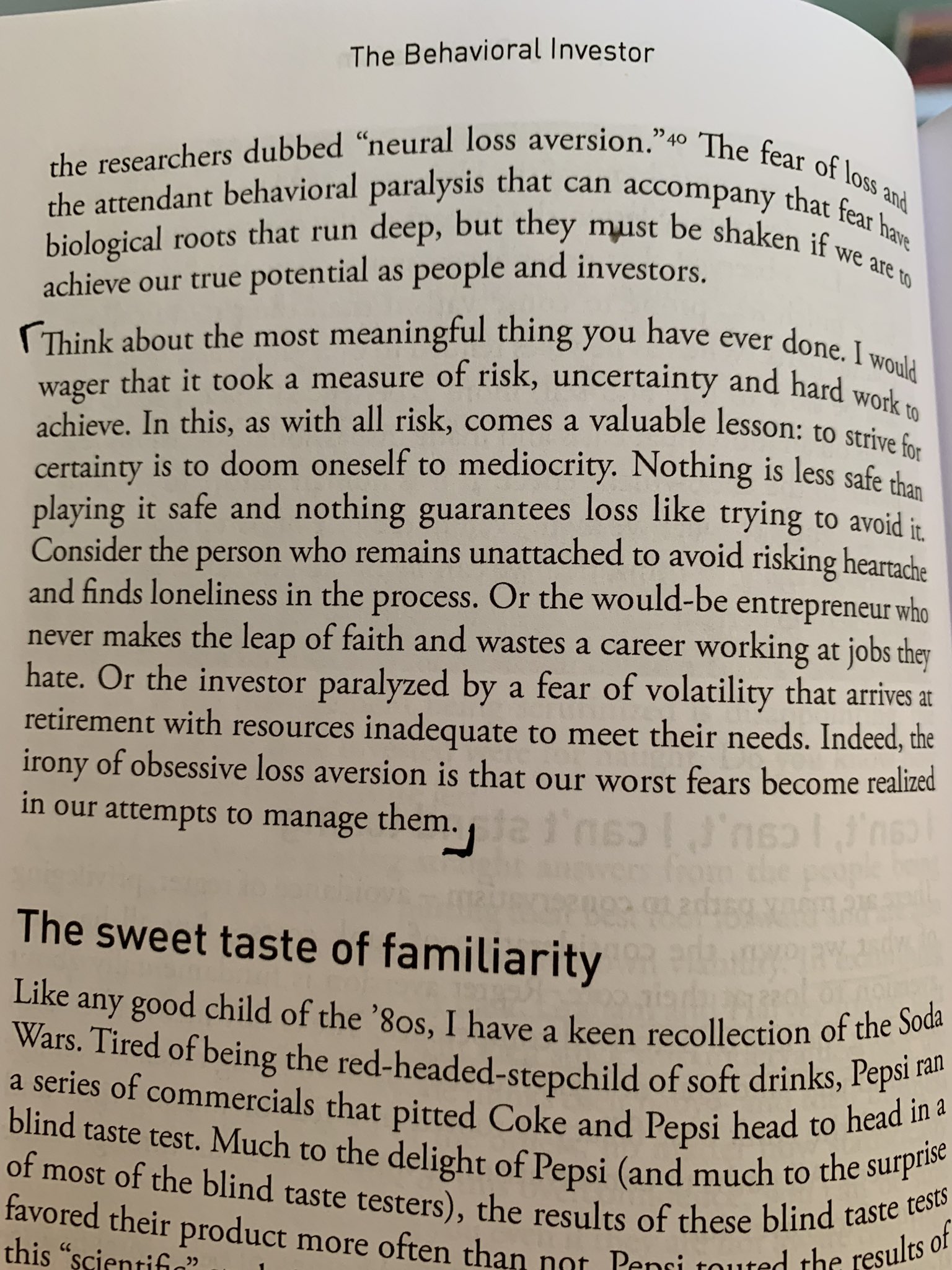

The same goes for investing. Learning to score your investment wins and losses based on the quality of your decisions and not on the quality of the outcome is key to managing your emotions, appropriately measuring your own performance and living to fight another day"

- Daniel Crosby (The Behavioral Investor)

Unfortunately, the investment community does not even come close to using the above logic. Advisers, investors and fund managers are too busy consulting the latest Morningstar 1 year performance numbers. Asset managers will tell you that they don't care about short-term performance but they are lying. That Morningstar report (or similar reports) is what pays the bills. In my experience, it is typically the funds near the top of the list that collect most of the assets under management. If your funds languish at the bottom of the pile, you can prepare yourself for some hefty outflows. There is an old saying that "performance sells".

What I believe Daniel Crosby is saying is the "process should sell". Investing success is not just a game of skill. It involves quite a bit of luck. Research (which Crosby discusses in book) shows that games that incur a high degree of luck as opposed to skill are best served by a rule-based or process driven approach. He points out "Winning a skill-based game like chess or basketball requires ... practice. Tasks with a significant degree of luck require a different discipline altogether ... what matters in a game of chance is not the outcome of any particular event, but the quality of your decisions."

So what does this all mean for you, the investor?

Stop worrying about your annual investment performance and start worrying about the process you follow. Do you have the right long-term asset allocation? Do you have a plan in place that you follow through all the ups and downs of the market?

My suggested plan is the same as always...

- Invest your money in real assets (property, shares etc - if South Africa goes south, ZAR cash isn't going to worth very much. I feel real assets have a better chance of maintaining purchasing power.)

- Build an offshore store of wealth or investment portfolio (heck, if you want to leave, it can be the start of you saving towards one of those Visa's you can buy in some European countries)

- Have access to offshore cash in hard currency (USD, EUR or GBP). If you need to get on a plane then you have some rent and food money.

- Start meditating (I am serious). Learn to deal with stress/anger that uncertainty in South Africa is causing you.

- Lastly, on a sunny African day go for a walk on the promenade at your nearest beach and wonder is it all really that bad...

And if that doesn't help, I have upgraded our pony to a unicorn...